Todas las entradas

Resumen del seminario web: «Happy CSRD: de la limitación a la oportunidad estratégica»

This summary contains key information from our webinar on 23 January 2025 dedicated to the Corporate Sustainability Reporting Directive and hosted by Rémi Postic. Rémi has been a partner at ERA Group since 2021 and specialises in working with clients involved in CSR, providing them with both a systemic vision and pragmatic action on the ground. Here are his explanations and advice on how to effectively finance and launch this initiative within your organization. >> To view the recording of the webinar (duration: 30 minutes), click here.

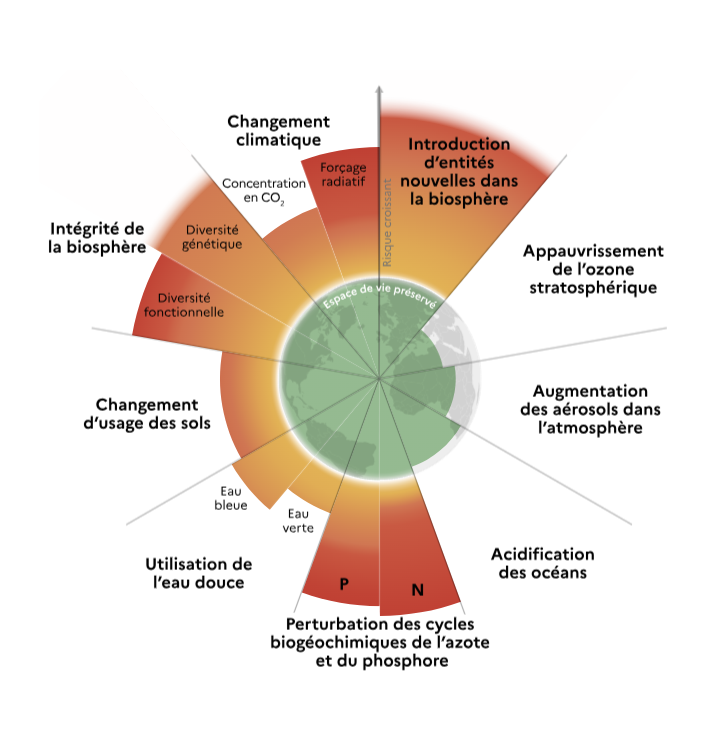

Six planetary boundaries have already been crossed out of the nine analyzed by the latest scientific research.

Climate change is one of them, for which the level of risk to our societies and lifestyles has been assessed according to the extent of global warming: we now know that we will be impacted even if we manage to keep global warming below the 1.5˚C threshold.

This is the case with ISO standards, including ISO 14 001, particularly in France. At the global level, in 2015 the United Nations adopted 17 Sustainable Development Goals (SDGs) aimed at eradicating poverty, supporting world peace and protecting the planet. Countries and many companies have committed to advancing the SDGs at their level.

The Corporate Sustainability Reporting Directive is the new reporting tool for companies, in force since 2024 within the European Union. It is part of the European Green Deal and specifically serves the "green finance" pillar. It thus helps to redirect capital flows towards a more sustainable economy and to integrate sustainability into risk management.

Listed companies are already applying it. Mid-sized companies have been subject to it since 2025. It is not currently mandatory for smaller companies, which are nevertheless affected by this directive as subcontractors of companies subject to the CSRD – and must therefore apply it to their entire value chain.

Like financial reports, CSRD reports are standardised and divided into standards and chapters, enabling companies to be analyzed, evaluated and compared with one another.

CSRD reporting comprises over 1,000 points, but the aim for companies is not to provide information on all of them. The aim is to help them broaden their scope of analysis by incorporating the principle of double materiality and the role of governance bodies.Our advice: choose the 10 to 100 key indicators for YOUR company, corresponding to your impacts and those of your value chain according to your activities and the size of your organization.

It is a valuable document for your financial partners: bankers, insurers, investment funds, shareholders, etc. This report gives them access to more information about your company, of an intangible nature. The value of your company will therefore no longer be based solely on financial aspects, but also on extra-financial aspects.

According to a 2024 estimate by the Court of Auditors, the investment is in the order of €50 to €500,000 per year. We recommend allocating 1% of your turnover to your CSRD/CSR budget for the entire process: the report as well as the transformation actions.

Take action with the three deliverables in our Starter Pack: